In the world of fixed income, yield is not everything. Nor is a solid credit rating.

Hidden risks can still erode your returns—and structural subordination is one of the most overlooked.

It is not about whether your bond is “senior” or “secured.” Structural subordination has nothing to do with the legal terms of the bond itself. Instead, it is baked into the corporate structure of the issuer. And in a stress scenario, it could mean you’re standing at the back of the line when the assets are handed out.

For ultra-wealthy families venturing into complex alternatives, direct deals, and private credit, understanding this risk isn’t optional. It is a must.

HoldCo vs OpCo: Why Your Place in the Structure Matters

Let’s say you buy a bond issued by a holding company (HoldCo). That company owns several operating subsidiaries (OpCos). The OpCos run the actual business, generate the cash, and own the valuable assets. The HoldCo? It is mostly a shell—its only real asset is equity in the OpCos.

So what happens if things go wrong?

OpCo creditors—whether lenders, suppliers, landlords, or litigants—get paid first, directly from the OpCo’s assets. Only after they have been satisfied does anything flow upstream to the HoldCo. That means HoldCo bondholders are effectively at the mercy of the OpCos’ financial health and liabilities.

Even if you are holding “senior unsecured notes” from the HoldCo, you are still structurally junior to everyone owed money by the OpCos.

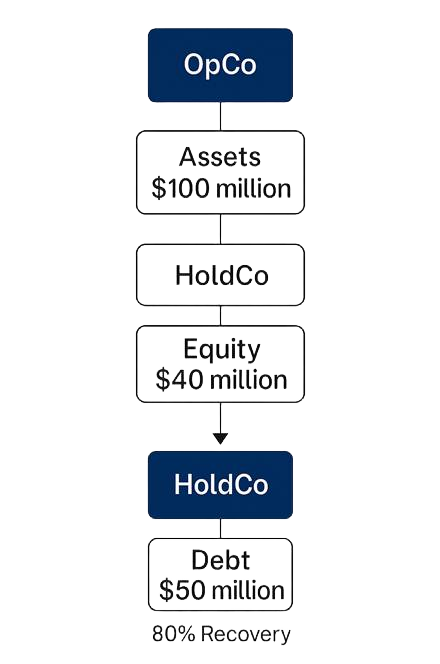

A Quick Example: Same Group, Different Outcomes

Imagine this setup:

- An OpCo has $100 million in assets and $60 million in debt.

- A HoldCo owns 100% of that OpCo and has $50 million in debt of its own.

Now assume liquidation.

The OpCo’s creditors get their $60 million first, leaving $40 million of equity value. That flows up to the HoldCo. But since the HoldCo owes $50 million, there’s not enough to go around. Its bondholders recover just 80%.

Same group. Same overall assets. Very different recovery outcomes—just because of where you sit in the structure.

Table: Common Bond Risks and Their Implications

Risk Type | Brief Description | Key Indicators in Prospectus | Potential Impact on Investors |

Credit Risk | Issuer may fail to make interest or principal payments. | Credit ratings (e.g., Moody’s, S&P), financial statements, discussion of issuer’s financial health. | Loss of interest income, partial or complete loss of principal. |

Interest Rate Risk | Bond’s value may decline due to rising market interest rates. | Maturity date, duration of the bond, discussion of interest rate sensitivity. | Potential capital loss if bond needs to be sold before maturity. |

Inflation Risk | Purchasing power of bond’s returns may be eroded by inflation. | Discussion of inflation and its potential impact, mention of inflation-protected securities (TIPS). | Real return may be lower than expected, potential loss of purchasing power. |

Liquidity Risk | Difficulty in selling the bond quickly at a fair price. | Credit rating, size of the bond issue, trading volume of similar bonds. | May have to sell at a discounted price or may not be able to sell when needed. |

Call Risk | Issuer may redeem the bond before maturity, typically when interest rates fall. | Call provisions, call protection period, discussion of issuer’s right to call the bond. | Reinvestment of principal at potentially lower interest rates, loss of expected future interest payments. |

Learning from the Past: Cautionary Tales

If the theory feels distant, history offers more than enough evidence of how structural subordination can bite — and bite hard.

Lehman Brothers

When the bank collapsed, creditors quickly discovered that not all claims were created equal. The web of subsidiaries and intercompany lending blurred recovery lines, leaving HoldCo creditors at the mercy of foreign insolvency regimes and prolonged litigation. Some waited over a decade to see partial repayments.

Country Garden (China’s Property Crisis)

Once viewed as one of China’s more conservative and financially sound developers, Country Garden’s fall from grace sent shockwaves through Asia’s credit markets. For offshore bondholders—many of them private clients and family offices in Hong Kong and Singapore—the pain was amplified by structural subordination.

Most of Country Garden’s offshore bonds were issued by holding companies registered outside mainland China, such as Country Garden Holdings Company Ltd in the Cayman Islands. Meanwhile, the bulk of its assets—land, projects, and cash flow—were held within dozens of mainland subsidiaries. When the company ran into liquidity trouble, onshore creditors, including state-owned banks and local suppliers, had direct claims on those operating entities. Offshore bondholders, by contrast, stood behind the firewall of China’s capital controls and legal system, with no direct recourse to the underlying assets.

In practice, this meant offshore creditors could not easily enforce claims or seize assets, and any recovery would be dependent on what remained after onshore claims were satisfied. Unlike in a unified bankruptcy proceeding, legal recourse was fragmented, and offshore claims became structurally subordinated by jurisdictional reality. Creditors holding bonds that once yielded 7–9% found themselves locked into protracted negotiations, facing uncertain recoveries and minimal transparency.

These case studies reinforce a harsh lesson: when you invest in a holding company with no direct asset ownership or cash flows, you are last in line—even if the coupon seems attractive.

Before you commit, make sure you’re asking the right questions.

Start here: the Subordination Risk Checklist Every Investor Should Know (hyperlink Article 10)